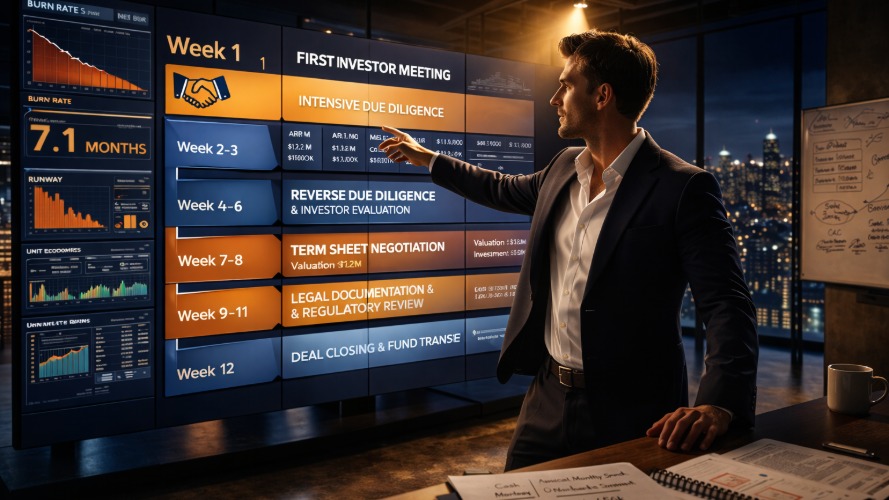

Successful MENA startups typically close funding rounds within 12 weeks of initial investor contact, though Saudi deals extend to 16 weeks due to regulatory requirements. This comprehensive timeline breaks down each phase from first meetings through deal closing.

Raising capital is one of the most demanding processes a founder will ever navigate. It is not just about having a great product or a compelling pitch. It is about understanding that fundraising is a structured process with predictable stages, specific activities at each step, and common friction points that derail even strong companies. The founders who close rounds consistently are not necessarily the ones with the best businesses. They are the ones who understand the timeline, manage the process professionally, and know exactly what to do at every stage of the journey.

This roadmap covers the complete 12 week fundraising process for MENA startups, with specific adjustments for Saudi Arabia where timelines extend to 16 weeks, UAE where processes move faster, and Pakistan where conditions vary significantly based on investor sophistication and regulatory environment.

The first meeting is not a pitch. It is a conversation designed to establish mutual interest and determine whether it makes sense for both parties to invest time in a deeper evaluation. Founders who treat the first meeting as a closing opportunity almost always damage their chances before due diligence begins.

What happens in week one is straightforward. You get in the room, make your case for the market opportunity, demonstrate that your team is capable of executing, and show early evidence that your thesis is correct. Investors in this meeting are not evaluating every detail of your financial model. They are asking themselves three questions. Is this market real and large enough to matter. Is this team capable of building something significant. Is the timing right for this idea.

What you should do in week one is focus entirely on the problem you are solving and the scale of the opportunity. Lead with market insight rather than product features. Show traction even if it is early and qualitative. Prepare a tight 12 to 15 slide deck that tells a clear story without overwhelming the room. Most importantly, treat the conversation as a two way evaluation from the very beginning.

What investors are doing in week one is taking notes on team dynamics, founder clarity, and market positioning. They are also beginning informal reference checks and discussing the opportunity internally with partners or analysts.

Common delays at this stage include unclear market positioning that leaves investors uncertain about the opportunity size, founders who present feature lists instead of market narratives, and misalignment on check size or stage fit that should have been identified before the meeting was scheduled.

If the first meeting generated genuine interest, the investor moves into formal due diligence. This phase is where most deals slow down or quietly fall apart, and it is almost always because founders were not prepared for the depth of scrutiny involved.

What happens in weeks two and three is intensive examination of your financial projections, customer acquisition model, unit economics, competitive landscape, and team background. Investors will request access to your data room and begin working through documents systematically.

What you should do is maintain a comprehensive and organized data room that includes at minimum your last 12 months of financial statements, monthly recurring revenue data broken down by customer, customer acquisition cost calculations with supporting data, lifetime value analysis, your cap table, key customer contracts, team CVs, and any existing legal agreements. Respond to every information request within 24 hours without exception. Founders who respond slowly signal operational dysfunction that investors extrapolate across the entire business.

What investors are doing is running financial analysis, calling customer references, researching competitors, and pressure testing your market size assumptions. They are also beginning to form a view on valuation based on comparable transactions and your current metrics.

Common delays include incomplete financial records, customers who give lukewarm references, revenue recognition policies that are unclear or aggressive, and customer concentration risk where one or two clients represent a disproportionate share of revenue. Founders should resolve all of these issues before fundraising begins rather than trying to explain them mid process.

This phase is where inexperienced founders make one of their most costly mistakes. They spend weeks two through six entirely focused on satisfying investor requests and forget to evaluate whether the investor sitting across from them is actually the right partner for their business.

What happens in weeks four through six is a parallel process. The investor continues their evaluation while you conduct your own structured assessment of them. This is not optional. The investor you take money from will have formal rights in your company and an informal influence on your culture, your future fundraises, and your strategic decisions for years.

What you should do is speak directly with founders at three to five of the investor's existing portfolio companies. Ask them specific questions about how the investor behaved during difficult periods, how responsive they are between board meetings, whether they opened doors they promised to open, and whether they would take money from this investor again. Also examine the investor's follow on investment patterns, their average check size relative to their fund size, and their typical board involvement level.

What investors are doing during this phase is completing reference checks on your team, finalizing their internal investment thesis, and beginning preliminary valuation discussions with partners.

Regional differences become particularly significant here. UAE based investors typically move efficiently through this phase due to their familiarity with international deal structures and established legal frameworks. Saudi investors may begin requesting documentation related to Vision 2030 alignment, local content requirements, and government partnership potential, all of which add time but also signal serious intent. Pakistani investors tend to focus heavily on local market validation, existing distribution partnerships, and evidence of the business model working within the specific constraints of the local economy.

The term sheet is where the deal takes its fundamental shape. Everything negotiated here will follow your company through its entire lifecycle, affecting future fundraises, founder liquidity, and exit economics in ways that are not always obvious in the moment.

What happens in weeks seven and eight is the investor presents a term sheet outlining the key commercial and governance terms of the investment. This document covers valuation, investment amount, liquidation preferences, anti dilution provisions, board composition, information rights, and protective provisions that give investors veto power over certain company decisions.

What you should do is engage an experienced startup attorney before you receive the term sheet, not after. Many founders make the mistake of reviewing the term sheet themselves first and only bringing in legal counsel once they have already formed opinions or made informal commitments. Your attorney should review every provision with specific attention to liquidation preferences, which determine how proceeds are distributed in an exit, and participation rights, which allow investors to receive their preferred return and then participate further in remaining proceeds.

Focus your negotiation energy on the terms that matter most over the long term. Valuation matters but it is not the only thing that matters. A high valuation with aggressive liquidation preferences and heavy protective provisions can leave founders with less economic upside and less operational freedom than a lower valuation with clean standard terms.

What investors are doing is finalizing their internal approval process, getting partner sign off on the proposed terms, and preparing for negotiation on points they expect founders to push back on.

Saudi term sheets frequently include additional provisions related to government incentive programs, Saudization requirements, and technology transfer obligations that require careful review by counsel familiar with local regulations. UAE negotiations generally follow international venture capital standards with modifications for local corporate law, making them more predictable for founders with international experience. Pakistani term sheets often include currency hedging provisions, restrictions on dividend repatriation, and exit timing clauses that reflect the regulatory environment and currency volatility unique to that market.

The legal phase is where many founders underestimate both the time required and the cost involved. It is also the phase where deals that seemed certain occasionally fall apart due to issues that should have been identified and resolved months earlier.

What happens in weeks nine through eleven is the drafting and negotiation of definitive legal agreements including the subscription agreement, shareholders agreement, and board resolutions. This phase also involves final regulatory filings and any government approvals required by the specific jurisdiction.

What you should do is ensure your corporate records are completely current before this phase begins. Outstanding legal issues, undocumented agreements with early employees or advisors, missing board approvals for previous decisions, or inconsistencies in your cap table will all surface here and create delays that frustrate investors and consume management time that should be spent running the business. Legal costs for this phase typically range from $15,000 to $50,000 depending on deal complexity and jurisdiction.

What investors are doing is conducting final verification of representations made throughout the process and working with their own counsel to protect their interests in the definitive documents.

Saudi Arabia extends the overall timeline to 16 weeks primarily because of this phase. Foreign investment transactions require review and approval from the Saudi Arabian General Investment Authority, and deals involving sectors designated as strategically sensitive face additional government scrutiny. Local content requirements and technology transfer obligations must be formally documented and approved. Founders raising in Saudi Arabia should factor this extended legal phase into their runway calculations and begin the process earlier than they would in other markets.

UAE deals benefit from established free zone structures in the Dubai International Financial Centre and Abu Dhabi Global Market that provide streamlined regulatory processes and internationally recognized legal frameworks. However mainland UAE deals involving entities outside the free zones require additional approvals that can add two to four weeks to the process.

Pakistani deals require State Bank of Pakistan approval for foreign currency investment transactions, which adds unpredictable timing to the closing process. Working with local counsel who has an established relationship with the relevant regulatory bodies is essential for managing this phase efficiently.

Closing week is simultaneously the most satisfying and the most logistically demanding week of the entire process. Multiple parties must coordinate across legal, financial, and administrative workstreams to execute all closing conditions simultaneously.

What happens in week twelve is the satisfaction of all conditions precedent specified in the term sheet, execution of all definitive legal documents, regulatory filings, and the actual wire transfer of funds to your company account. Final board resolutions authorizing the share issuance must be prepared and executed, updated cap table documentation must be confirmed by all parties, and proof of required corporate insurance must be provided.

What you should do is prepare a detailed closing checklist at least three weeks before the expected closing date and assign clear ownership of every item on that list. The most common reason closings slip from week twelve into weeks thirteen or fourteen is coordination failure rather than substantive disagreement. Know exactly what needs to happen, who is responsible for each item, and what the dependencies are between tasks.

Investor ghosting typically begins between weeks three and five and is one of the most psychologically difficult aspects of the fundraising process. The professional response to ghosting is not repeated follow up messages but rather a single clear and direct communication that creates a deadline for response. Something along the lines of noting that you are moving forward with your process and would appreciate knowing whether they are still interested by a specific date is far more effective than multiple check in messages that signal desperation.

Lowball term sheets should be evaluated against your actual alternatives rather than your hoped for valuation. If you have competing investor interest, reference it professionally and specifically. If you do not, assess whether the terms offered allow you to build the business you are trying to build and whether the investor brings enough strategic value to justify a lower headline number. Never reject a term sheet without understanding your alternatives clearly.

Investors who demand exclusive negotiation periods of more than four weeks without a committed timeline are signaling process problems. Investors who request control provisions that significantly exceed market standards are signaling misalignment on founder autonomy. Investors who demonstrate limited understanding of the regulatory environment in which they claim to operate are signaling execution risk that will surface at the worst possible moments. Any investor who behaves unprofessionally during the fundraising process will behave worse once they have formal rights in your company. Trust that signal completely.

Fundraising is hard for every founder regardless of how strong their business is. The ones who navigate it successfully are not the ones who avoid the difficult moments but the ones who understand the process well enough to see those moments coming and respond to them with clarity, professionalism, and preparation. This roadmap gives you the map. What happens next depends entirely on how well you run the journey.